The 10 Best Countries to Open an Offshore Bank Account in 2026

22 Jun 2026

Key Takeaways

- There's no single best country to open an offshore bank account - but for most international businesses, three names do the heavy lifting: Panama, the British Virgin Islands, and the Cayman Islands.

- Panama is the standout for operating businesses: its territorial tax system leaves foreign-earned income untaxed, and its USD economy removes currency friction for anyone with US-linked operations.

- The BVI pairs zero corporate and capital gains tax with English common law and strong confidentiality, making it a go-to for holding companies and international structures (note it's currently FATF grey-listed and working through remediation).

- The Cayman Islands is the tax-neutral gold standard for funds and serious wealth - no income, capital gains, or corporate tax, backed by tight, credible regulation.

- Beyond these three, Seychelles offers the cheapest entry (often no minimum deposit), Georgia the fastest setup, and Singapore or a US LLC the most global credibility.

- Wherever you bank, regulatory standing and proper reporting (CRS/FATCA) matter - offshore is about legitimate diversification and tax efficiency, not secrecy.

What Is an Offshore Bank Account (and Why People Actually Open One)?

An offshore bank account is simply an account held in a country where you don't live. That's it - there's nothing inherently secretive or shady about it, despite the reputation. A Canadian founder with an account in Singapore, or a German consultant banking through a US LLC, both hold offshore accounts.

People open them for practical reasons. Asset protection is a big one: spreading your money across more than one legal system means a single lawsuit, bank failure, or political shock at home can't freeze everything you have. Multi-currency access lets you hold and move USD, EUR, GBP, and more without bleeding money on conversions. Tax efficiency is a legitimate driver too, when structured correctly and declared properly. And many people simply want privacy and diversification - not to hide, but to avoid having their entire financial life sitting inside one banking system.

When you compare the best offshore bank accounts, you're really comparing how well a jurisdiction delivers on those needs. The rest of this guide breaks that down country by country.

How to Pick the Right Offshore Banking Jurisdiction for You

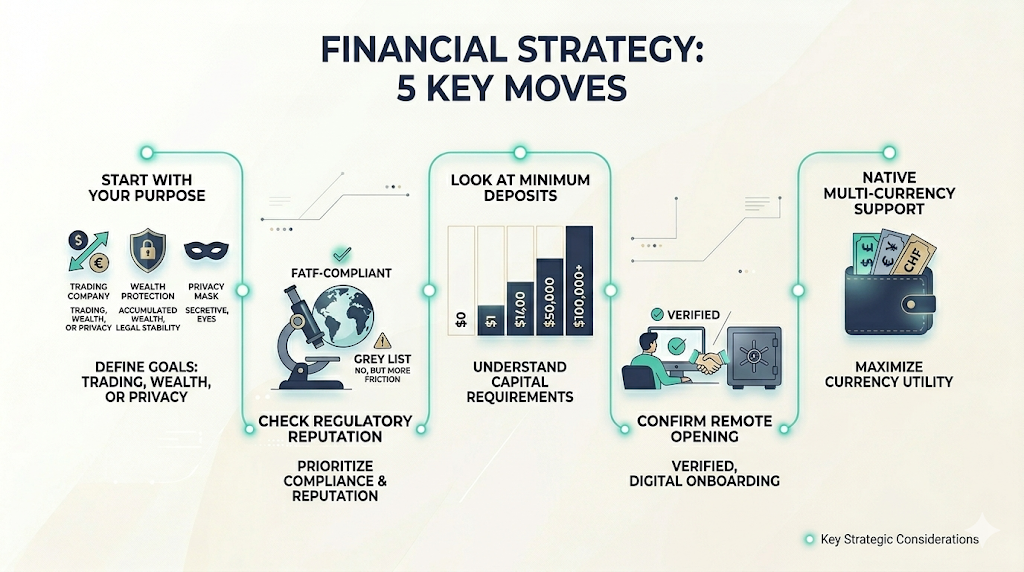

Most guides hand you a generic checklist. Here's the advice version instead - the five things that actually move the needle.

Start With Uour Purpose.

Trading internationally, protecting accumulated wealth, and wanting privacy are three different goals, and they point to different places. A trading company wants strong payment rails and multi-currency support; someone protecting wealth wants stability and a solid legal system.

Check the Jurisdiction's Regulatory Reputation

This is the step people skip. Look at whether the country is FATF-compliant and whether it currently sits on the FATF "grey list" of jurisdictions under increased monitoring. Grey-listing isn't a sanction and doesn't make banking there illegal, but it can mean more friction and more scrutiny from counterparties. Among offshore banking countries, reputation is part of the product you're buying.

Look Hard at Minimum Deposit Requirements

These range from effectively zero to six figures. Don't lock up capital you need elsewhere.

Confirm whether remote opening is truly possible

Not "technically offered" but actually achievable for someone in your situation. Many traditional banks still want you in the room; fintech platforms increasingly don't.

Finally, multi-currency support

If you earn in several currencies, an account that holds them natively saves real money over time.

British Virgin Islands (BVI) - Strong Privacy and Zero Corporate Tax

The BVI has been a cornerstone of offshore finance for decades, and the appeal is straightforward: there's no corporate income tax, no capital gains tax, and the jurisdiction has long offered strong confidentiality for company ownership. It runs on English common law, which gives international businesses a familiar and predictable legal footing. For holding structures and international business companies, it remains one of the most widely used names on this list.

Be aware of one current development, though. In June 2025 the FATF added the BVI to its grey list of jurisdictions under increased monitoring, and it remained there going into 2026. This is not a blacklist - it imposes no sanctions and doesn't make BVI banking illegal - but it signals the territory is working to strengthen its anti-money-laundering framework, a process it expects to take around two years. Practically, expect somewhat more diligence from banks and partners while that plays out. The privacy and tax advantages are real; just go in with eyes open.

Best for: holding companies and international structures that value common-law familiarity and confidentiality.

Panama - Territorial Taxation and Asset Protection

Panama's headline advantage is its territorial tax system: income earned outside Panama generally isn't taxed locally. For a business operating internationally, that's a genuinely powerful feature, not a marketing line. Panama also runs a USD-based economy, which removes foreign-exchange friction for anyone with US-linked operations - you're banking in dollars from day one.

The honest caveats matter here. Opening an account typically requires either an in-person visit or a local legal representative, so it's not a fully remote, open-from-your-laptop affair. And since the Panama Papers fallout, KYC and AML requirements have tightened considerably - compliance is more demanding than it was a decade ago, and banks will want a clear picture of your business and source of funds. None of this is disqualifying; it just means setting realistic expectations on timeline and paperwork.

Best for: Latin America-focused businesses and US-based entrepreneurs who want a dollar-denominated base with territorial tax treatment.

Cayman Islands - Tax-Neutral Jurisdiction for Global Business

Cayman deserves to be understood as a serious financial centre, not a cliché tax haven. As a tax-neutral jurisdiction, it levies no income tax, no capital gains tax, and no corporate tax - and it backs that up with English common law and a tightly regulated banking sector. That regulation is a feature, not a bug: it's part of why Cayman carries credibility with institutional counterparties that more obscure jurisdictions don't. Notably, Cayman was removed from the FATF grey list in 2023, which further strengthened its standing.

The downsides are real and worth stating plainly. Minimum deposits tend to be high, account setup is usually in-person, and the whole ecosystem is built around investment funds and high-net-worth individuals rather than small businesses. If you're a solo founder with modest balances, Cayman is probably overkill. If you're running a fund or managing substantial assets, it's close to ideal.

Best for: investment funds, holding structures, and high-net-worth individuals who want a credible, tax-neutral base.

Seychelles - Low-Cost Setup and Business Privacy

Seychelles is underrated, and most guides don't explain why. Setup costs are low, foreign-sourced income isn't taxed, and the jurisdiction actively supports international business companies and offshore structures. Crucially for newer businesses, remote account opening is available through licensed service providers, and some options come with little or no minimum balance - making it one of the few realistic routes to an offshore bank account with no minimum deposit.

The trade-off is scale. The Seychelles banking ecosystem is smaller and less sophisticated than Singapore's or Hong Kong's. If you need cutting-edge fintech, complex investment products, or deep capital-markets access, this isn't your jurisdiction. But if you're getting started and want a cost-effective, low-friction entry into offshore banking, Seychelles punches above its weight.

Best for: early-stage businesses and entrepreneurs looking for a cost-effective entry point into offshore banking.

United Arab Emirates (UAE) - Modern Business Hub With Tax Benefits

The UAE has gone from "nice to have" to a genuine top-tier offshore banking destination. The free-zone structure allows 100% foreign ownership, there's no personal income tax, and the digital banking infrastructure is improving quickly. On the corporate side, be precise about the tax picture: the UAE introduced a 9% federal corporate tax (on profits above AED 375,000) effective from 2023, but a Qualifying Free Zone Person can still pay 0% on qualifying income if it meets the conditions. So it's "zero tax on the right income," not "zero tax across the board" - an important distinction the older guides get wrong.

On banking, the main names are Emirates NBD (large network and strong digital tools), RAK Bank (popular with SMEs and free-zone companies), and ADCB (solid corporate offering). Most traditional UAE banks still prefer in-person setup, though digital platforms are steadily chipping away at that. The UAE is especially strong if you're targeting Middle East, Africa, and South Asia markets.

Best for: internationally minded businesses wanting a modern hub with access to MEASA markets.

Georgia - Low Taxes and Easy Company Setup

Georgia is the surprise entry that competitors mention but rarely explain. Its biggest selling point is speed and simplicity: accounts can often be opened within a couple of business days, and the process is refreshingly non-bureaucratic. Taxes are genuinely low, the main banks - Bank of Georgia and TBC Bank - offer multi-currency accounts and solid online banking, and Georgian banks have historically offered attractive local-currency deposit rates for those chasing yield. Privacy is reasonable, and the whole experience tends to be faster than the bigger names.

There's one honest downside. Georgia doesn't carry the prestige of Singapore or Switzerland, so counterparties in certain industries may look at a Georgian bank address with a bit more scrutiny. For most entrepreneurs and digital nomads - particularly US citizens who value flexibility and don't want to wait weeks - that's a small price for how quick and painless the process is.

Best for: cost-conscious entrepreneurs and US citizens who value speed and simplicity.

Singapore - World-Class Banking and Business Reputation

Singapore is the gold standard, and there's no need to hedge about it. Regulated by the Monetary Authority of Singapore (MAS), it hosts a banking ecosystem of more than 150 banks, including heavyweights like DBS, OCBC, UOB, and HSBC. The practical advantages are excellent: native multi-currency accounts, strong international payment rails, and some of the best digital banking anywhere. When people rank the best offshore bank accounts by overall quality and credibility, Singapore is almost always near the top.

The honest downside is that compliance is thorough. Expect detailed questions about your source of funds and the rationale behind your business - MAS-regulated banks take onboarding seriously. Traditional banks usually require an in-person visit, although fintech platforms now offer fully remote onboarding, often with no minimum deposit. The diligence is the flip side of the credibility; you can't really have one without the other.

Best for: SMEs, holding companies, digital businesses, and anyone who wants maximum credibility with counterparties.

Hong Kong - Gateway to Asian Markets

If you have trade ties to mainland China or the broader region, Hong Kong is hard to beat. Its concentration of major banks is exceptional - more than 70 of the world's largest 100 banks have a presence here - and multi-currency accounts supporting HKD, USD, and CNY are a major draw for anyone moving money across Asia. As one of the premier offshore banking countries for Asian trade, its infrastructure is genuinely world-class.

Be transparent about the friction, though. Non-resident account opening has become noticeably harder since 2020, compliance is strict, and traditional banks frequently require an in-person visit. The good news is that fintech platforms now fill this gap effectively, offering routes to a Hong Kong account that don't depend on flying in and sitting across from a relationship manager. Go in expecting scrutiny and a clear business rationale, and Hong Kong rewards you with unmatched access to Asian markets.

Best for: businesses with trade links to China and the wider Asia-Pacific region.

Mauritius - Tax-Efficient International Business Hub

Mauritius is a smart, specific choice rather than a general-purpose one. Its real value lies in an extensive double-tax-treaty network - 45 treaties in force, covering major economies like India, China, South Africa, and the UAE - which is exactly what makes it strategically powerful for holding structures investing across Africa and Asia. If your business is built around the Africa–India corridor, few jurisdictions serve you better.

The main banks are MCB, AfrAsia, and Bank One, and remote onboarding is possible through intermediaries. The island is both English- and French-speaking, which is a practical advantage when dealing with Francophone African markets. Mauritius was removed from the FATF grey list back in 2021, so its compliance standing is solid. The key is to use it for what it's best at: treaty-driven holding structures with African or Indian exposure, not generic day-to-day business banking.

Best for: holding companies, African market expansion, and businesses that need favourable treaty access.

United States (LLC) - Flexible Structure and Global Credibility

This is the wildcard, and most guides ignore it. A US LLC - typically formed in Wyoming or Delaware - can function as a remarkably effective offshore structure for non-US residents. As a single-member LLC, it's treated as a disregarded "pass-through" entity, and a non-resident owner is generally taxed by the US only on income effectively connected to a US trade or business (ECI). If you run your operations from outside the US with no US office, employees, or dependent agents, your income typically isn't ECI - even when your clients are American.

The advantages are hard to overstate: unmatched global credibility, easy access to US payment processors, and banks and vendors worldwide that instantly recognise and trust a US entity. Two honest caveats. First, this tax treatment works for non-US residents - it does not apply the same way to US citizens. Second, "no entity tax" doesn't mean "no paperwork": a foreign-owned LLC must file Form 5472 with a pro forma 1120, plus a Beneficial Ownership Information (BOI) report. Manageable, but real.

Best for: non-US residents who want global credibility, smooth payments, and straightforward compliance.

Comparison: The 10 Jurisdictions at a Glance

Use this as a shortcut, then read the relevant section above before deciding. "Remote opening" reflects what's realistically achievable, often via fintech platforms even where traditional banks prefer an in-person visit.

A Quick Word on Compliance and Legality

Offshore banking is legal. What's not legal is hiding money to dodge taxes you owe. The distinction matters, and it's worth being clear-eyed about it before you open anything.

Under the Common Reporting Standard (CRS), most jurisdictions on this list automatically share account information with tax authorities in your home country, and US persons are covered separately by FATCA. In practice that means an offshore account is not a secret from your tax office - and it shouldn't be. You'll generally still need to declare the account and report income wherever you're tax-resident. Used properly, offshore banking is about diversification, asset protection, currency access, and legitimate tax efficiency. Used to conceal, it's a fast route to serious penalties. When the structure or the numbers get complex, get advice from a qualified cross-border tax professional before you act.

Frequently Asked Questions

Which country is best for opening an offshore bank account with no minimum deposit?

Seychelles is the standout for low- or no-minimum options through licensed providers, and fintech platforms in Singapore and the US can also open accounts with little to no minimum balance.

Can I open an offshore account remotely?

In several jurisdictions, yes - Georgia, Seychelles, and a US LLC are among the most remote-friendly, and fintech platforms increasingly enable remote onboarding even in Singapore and Hong Kong, where traditional banks still prefer an in-person visit.

Is offshore banking legal?

Yes, provided you declare the account and report income where you're tax-resident. CRS and FATCA mean these accounts are reported to tax authorities, so transparency is essential.

Which jurisdiction gives the most credibility with international partners?

Singapore and a US LLC carry the strongest global recognition, which smooths relationships with banks, payment processors, and vendors worldwide.

About the author

Pavle Sarcevic

Founder of Incorporify

Pavle is the founder of Incorporify, a company helping entrepreneurs and businesses set up offshore companies and navigate international structuring. With hands-on experience in global business formation, he specializes in jurisdiction selection, entity structuring, and helping clients expand beyond borders with the right legal and financial foundations.

Table of Contents

Your Offshore Company, Registered in 5–7 Days

One specialist handles your formation, banking, and compliance start to finish, fully remote.

2-min form · No cost · No obligation